Summary

The 2026 State of Scale-ups

Based on 200+ company completions, the data reveals the systemic structural pressures and operational "blind spots" of the modern scale-up landscape.

New to the PragmaPulse® framework? Jump straight to understanding the data →

Pillar Performance Overview ⓘ

Achilles Heel: Finance and Compliance

Finance and compliance is the weakest pillar. Nearly every finance element sits below the cohort average.

Succession: A Universal Blind Spot

Succession is consistently weak across all sectors and sizes. No sector scores above 5.0, pointing to an acute advisory gap with no clear market leader.

Digital Confidence is Real but Uneven

Data and IT is the strongest pillar, yet Business Intelligence and Managed Reporting lag significantly behind core business tool adoption.

Size Drives Maturity: Micro Gap

Micro firms (1–9 staff) score a full point below small firms. Finance and Operations are where the steepest performance shortfalls occur.

Intra-Company Alignment Fractures

69% of leaders within the same organisation diverge on their business health, proving that internal silos and "Critical Lens" perspectives are common.

Financial Services Sector Leads

Financial Services is the top-performing sector, yet even within this group, the Finance & Compliance Pillar remains a surprising structural weakness.

Framework

The PragmaPulse® Framework

Explore the complete data set mapping the holistic health of scaling businesses. Uncover structural priorities to build your pragmatic roadmap across all 42 modules.

What is the PragmaPulse® Diagnostic?

Growth often brings chaos. For scale-ups, moving fast can easily obscure structural weaknesses. Without a clear view of the entire operation, it becomes difficult to spot bottlenecks before they impact the bottom line or decide where to invest limited resources.

That is the purpose of the PragmaPulse® Diagnostic. It acts as a holistic assessment that pinpoints operational strengths and exposes hidden vulnerabilities across six core business pillars.

The companies included in this 2026 data cohort shared their data to uncover their own systemic blind spots and build a pragmatic roadmap for sustainable growth. In doing so, they have collectively mapped the reality of the modern scale-up landscape.

The aggregated data from this year's cohort reveals a stark contrast between where leaders believe they excel and where their businesses are structurally fragile. We have categorised the performance of each pillar below to provide a clear 'Health Heatmap'.

Decoding the Diagnostic: What do the scores actually mean?

To ground these numbers, it helps to overlay the scores against the maturity levels of the PragmaPulse® framework:

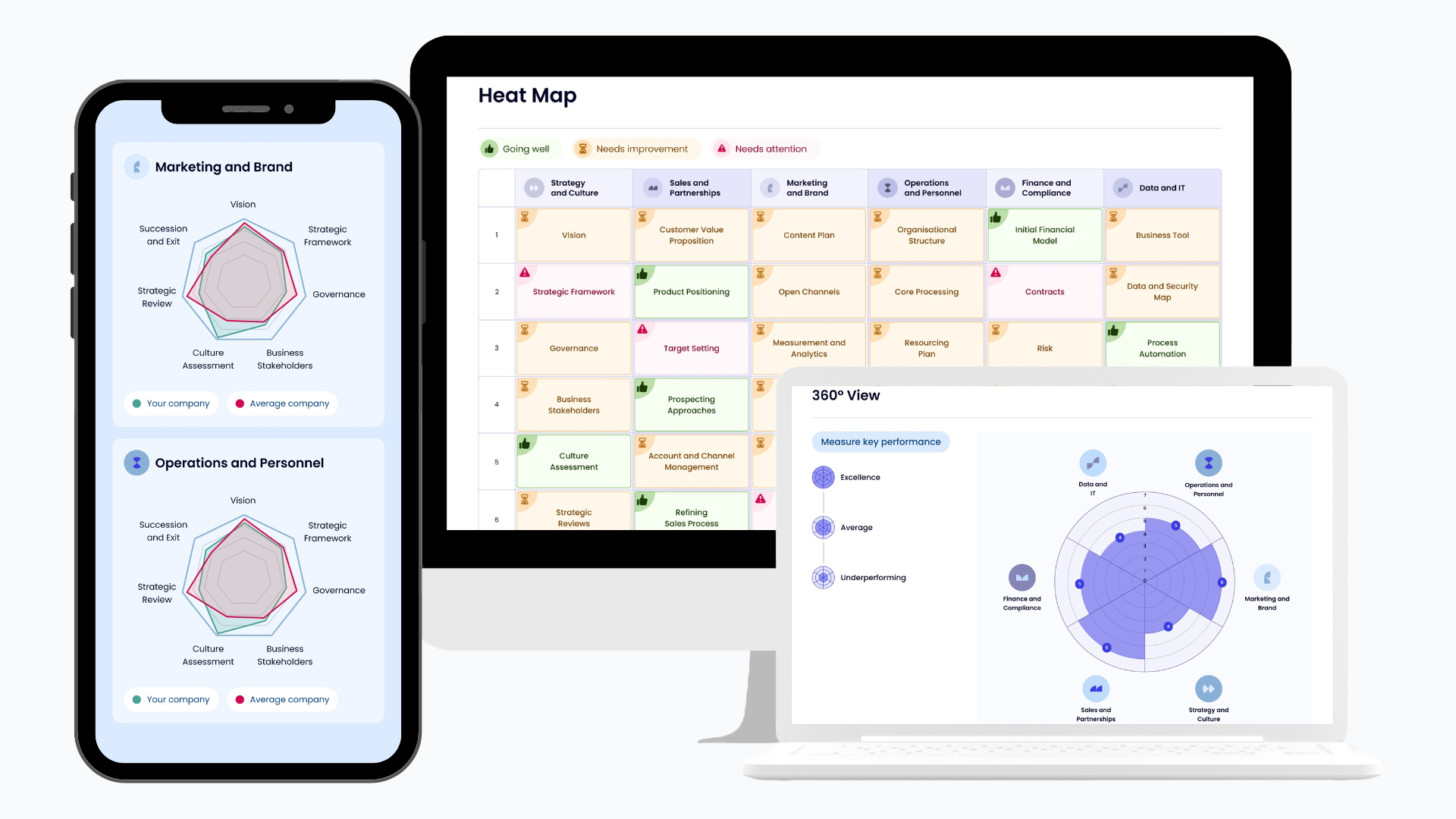

Heat Map

The Diagnostic Heatmap

Explore the aggregated performance across the full 42-module framework, or toggle the view to isolate the cohort's most critical gaps and top-performing strengths.

How should I read this?

This heatmap provides a high-level visual index of cohort performance across the 42 modules. Use it as a useful benchmark to see where market standards are established versus where collective gaps exist.

Why no excellence?

While 7% of individual module assessments across the cohort were rated as 'Excellence', the process of averaging multiple scores into a single cohort mean naturally pulls the results toward the centre.

How can I get this for my business?

PragmaPulse allows you to run this exact 42-module diagnostic for your own company. You can unlock your own roadmap and benchmarking by viewing the options at the bottom of this report.

Element Analysis: Strengths & Critical Gaps

Top and bottom 8 of 42 elements by mean score (0–10 scale)

Themes

Emergent Narratives

Three clear themes emerged from this year's data. First, a persistent gap between strategic ambition and day-to-day execution. Second, a widespread blind spot around exit readiness and long-term valuation. Third, a tendency to chase new technology at the expense of foundational disciplines. We explore each in turn.

The Strategy-Execution Gap

Amidst the turbulence of 2026, scale-ups are defiantly confident about charting their own course. Core, foundational activities like Vision and Strategic Frameworks rank among the highest in our entire data set. Leaders are comfortable painting a 'North Star', but the data gap reveals a distance between where leaders think their business is going and what is actually happening on the ground.

In a year once again dominated by talk of AI, this problem is distinctly human.

Why we love strategy (and avoid execution)

Psychologists have long documented what is sometimes called construal level theory: when we think about the future, we do so in abstract, high-level terms. Goals feel energising. Strategy sessions feel creative. Whiteboard sessions are where ideas get born and momentum feels real.

Execution is the opposite. It forces us down into the granular. The spreadsheet. The uncomfortable conversation with an underperforming team member. The process documentation nobody wants to write. Jeffrey Pfeffer and Robert Sutton spent years studying this precise phenomenon at Stanford. Their landmark work, The Knowing-Doing Gap, arrived at a blunt conclusion: most organisations know far more than they ever put into practice. The problem is never a shortage of knowledge. It is a cultural resistance to the hard, unglamorous work of doing.

Scale-ups are a particular breeding ground for this gap because founders are almost always pattern-matched as visionaries. That is how they secured funding. That is the version of themselves they present to the board. They are eminently capable of doing the work: building new systems, tracking operational KPIs, and reviewing sales processes. However, it's far easier to play in the world of high-level and what-if (not to mention more fun).

The result is a business running on founder instinct rather than systems and data.

Closing the Gap

Closing the gap is not about working harder; it's about changing the nature of the work. It requires a transition from the 'heroic' phase of growth, where success depends on individual brilliance, to the 'systemic' phase, where success is the predictable result of repeatable processes.

This shift is often uncomfortable for scale-up leaders because it demands a move from high-level vision to ground-level accountability. However, it is the only way to ensure that the 'North Star' isn't just a distant light, but a destination the entire organisation is systematically moving toward.

Based on our cohort data, there are a few specific, practical shifts that companies at the 4-6 execution maturity level tend to benefit from most:

Daily Alignment

Connect strategy to daily work using OKRs. Define key results with precision to remove ambiguity about achievement.

Data Reflex

Build a measurement culture before buying a tool. Ensure leaders start every meeting with data until it becomes a reflex.

Hire Operators

Accept that execution requires a different kind of leader. Hiring a COO or Head of Operations stops you being the bottleneck.

The Exit Blind Spot

Succession and Exit is the single lowest-scoring module across the entire 2026 cohort, sitting more than two full points below the highest-rated elements. That gap is significant, and it tells a story about how founders think about the future of their businesses.

Most leaders treat an exit as a distant event. Something to consider in five or ten years. A transaction that belongs at the end of the story, not in the middle of it. The data confirms this: the overwhelming majority of scale-ups in this cohort have done little to no formal exit planning.

"If I had treated exit readiness as a continuous discipline rather than a final project, that timeline could have been dramatically shorter. That experience is a large part of why Succession and Exit sits inside the PragmaPulse framework. It is not about wanting to leave. It is about building a business that does not need you to be in every room."

Why exit planning matters today

There is a compelling argument to be made that the process of building a sellable company is identical to the process of building a well-run one. When you design a business that can operate without you, you are forced to systematise operations, document processes, formalise governance, and build a leadership team that functions independently. These are not exit activities. They are good business practices that happen to make your company more valuable.

Research from the Exit Planning Institute reinforces this further. Their data consistently shows that owners who begin exit planning at least three to five years before a transition achieve significantly higher valuations than those who start reactively. The difference is not marginal. It is often 50 to 100 percent of the final sale price.

Yet in the PragmaPulse data, we see Maximising Valuation sitting at just 4.9 and Expansion Model at 5.1. These are the modules that directly determine exit value, and they rank among the very lowest in the entire dataset. A business that has not modelled its growth trajectory or mapped its valuation levers is a high-risk proposition for any buyer. It is also a fragile business to run day to day.

Reframing the exit

Many scale ups view exit planning as a kind of betrayal of their team or their mission. If I'm thinking about selling the company, doesn't that mean I don't believe in it anymore?

The reality is more nuanced. Building exit readiness is about building a more resilient, autonomous organisation. By operationalising the business to the point where it can be valued and transferred, leaders actually secure the legacy of their mission rather than abandoning it. It turns a fragile, founder-dependent entity into a robust asset that can thrive under new ownership or within a larger structure.

Building Exit Readiness

Building exit readiness is about building a more resilient, autonomous organisation. By operationalising the business to the point where it can be valued and transferred, leaders actually secure the legacy of their mission rather than abandoning it. It turns a fragile, founder-dependent entity into a robust asset that can thrive under new ownership or within a larger structure.

Reduce Founder Dependency

Document every process that currently lives in the founder's head. The business should be able to run for a month without you.

Formalise Governance

Establish a proper advisory board or non-executive structure. Buyers want to see decisions made through a system, not an individual.

Audit Your Contracts

Ensure all supplier, client, and employment contracts are current, documented, and transferable. Informal arrangements kill valuation.

Chasing Shiny Objects

The Data and IT pillar leads the 2026 cohort. Scale-ups are investing significant time and attention in new technology capabilities. The question is whether this represents genuine strategic advantage or a form of trend-chasing driven by market pressure. The data suggests it is often the latter.

The AI value gap

BCG's 2025 research, "The Widening AI Value Gap", found that just 5% of companies are successfully scaling AI to generate measurable financial returns. The remaining 95% are trapped in what researchers call "pilot purgatory": running experiments, building prototypes, and presenting demos that never translate into operational value. McKinsey's data tells a similar story. Around 88% of organisations now use AI in at least one function, yet only 6% report significant bottom-line impact.

The primary reason is not the technology. It is the foundation underneath it. AI models are only as reliable as the data they consume. If your data is unstructured, siloed, or incomplete, the outputs will reflect that. Our cohort data confirms the problem: Business Intelligence clocks in at just 5.8 - the lowest in the pillar. You cannot deploy sophisticated AI tools on top of disorganised information and expect consistent results.

The false confidence problem

There is a subtler risk here that the data hints at. When leaders report high confidence in their technology strategy while simultaneously scoring poorly on financial modelling and expansion planning, it suggests a dangerous disconnect. The confidence itself becomes the vulnerability.

A company that believes it is technologically advanced may deprioritise the operational basics. It may delay investing in its financial infrastructure because it feels modern. It may underestimate cyber risk because it has adopted the latest tools. The World Economic Forum has noted this pattern specifically: organisations that layer AI onto broken workflows often amplify existing inefficiencies rather than solving them.

Let's remember that our new AI friends themselves are particularly sycophantic creatures - they excel in telling us we are brilliant, regardless of the reality.

Making AI Work for the Boring Stuff

The most valuable application of AI for scale-ups at the 5.0 to 6.5 maturity range is not in building advanced capabilities. It is in strengthening the fundamentals they are currently neglecting.

Automate the Basics

Use AI to handle the unglamorous operational work: invoices, contract review, and transcription for immediate returns.

Fix Data First

Invest in data governance and structure first. One reliable source of truth outperforms a dozen AI experiments built on messy data.

Audit Your Priorities

If Data scores are strong but Financials lag, your allocation needs review. Solid fundamentals outlast market hype.

Focus

Industry Insights

We've next broken the data down over 6 distinct sectors, giving us an interesting glimpse under the hood at shared strengths and vulnerabilities by industry.

While industry-specific challenges exist, the data highlights a surprising amount of commonality across the cohort. The most successful scale-ups are those that look beyond their own sector's "standard" and adopt best practices from high-performing industries like Financial Services or Tech. Learning from these nuances is key to cross-pollinating operational excellence.

Focus

Growth Milestones

Data sliced by the scale and maturity of the business, proving that certain weaknesses are practically evolutionary milestones.

Growth is rarely linear. For "Micro" firms, the challenge is often the "founder bottleneck", tiny teams wearing every hat simultaneously. Interestingly, our data shows that "Small" companies (10-49) actually outperform "Medium" ones (50-249) in overall maturity. This proves that bigger doesn't always equal better; as businesses scale, they often introduce new complexities that can dilute the operational excellence seen in smaller, more agile teams.

Steps

Closing the Gap

Thank you for exploring the 2026 PragmaPulse® Cohort Report. This data is only possible thanks to the transparency and growth mindset of the hundreds of scaling businesses that share their diagnostic journey with us.

Want to see how your business stacks up?

You've just seen the pressure points across 200+ scale-ups. Now it's time to see your data.

While the cohort data provides a powerful benchmark, the true value of the PragmaPulse® Diagnostic lies in its application to your business.

- Bespoke Heatmap: Your specific 42-module score distribution.

- In-depth Benchmarking: See how you compare to industry peers.

- Pragmatic Roadmap: Automated priority mapping based on your scores.

- The Pulse Review: A guided session to turn data into a 90-day execution plan.